Can CoreWeave escape the landlord tax?

CoreWeave is signing impressive deals with hyperscalers; whether that revenue flows through to shareholders or landlords remains an open question

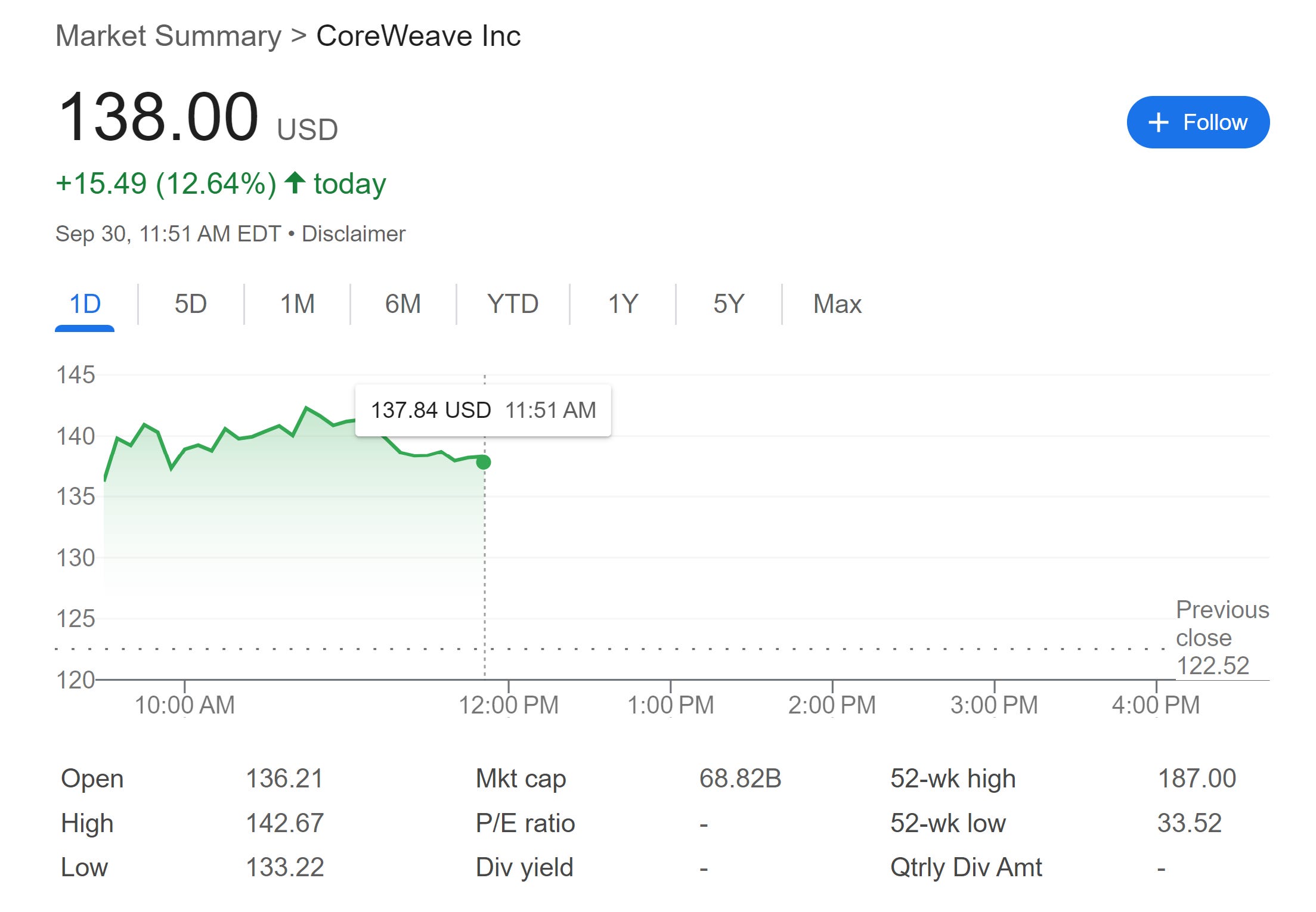

This past August, I wrote a fairly negative piece about CoreWeave. More recently, short seller Kerrisdale Capital released a jeremiad against the company. (I continue to hold no position in CoreWeave.) And, today CoreWeave announced a multibillion dollar partnership with Meta. Its stock popped.

So what’s going on?

My main criticism a…